Brian Klepper

Originally published 10/09/2018 in the Valid Points Newsletter

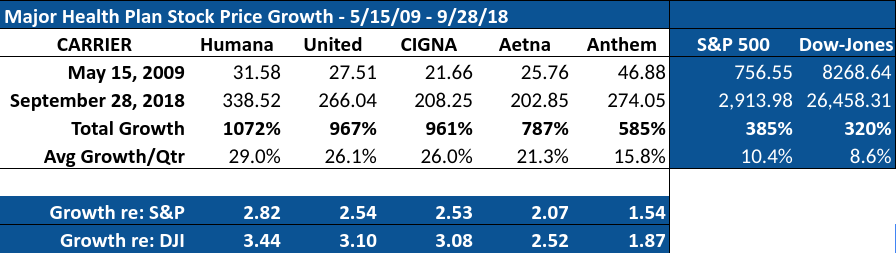

Below are calculations of major health plan stock price growth over a 37 quarter period between May 15, 2009 and September 28, 2018. Note that, during this time, the big plans’ stock price value skyrocketed between 585% and 1,072%, about 2.75x the growth of the Dow Jones Index and 2.25x the growth of the S&P. Humana and United have sustained a breathtaking average per quarter growth of 29.0% and 26.1% respectively.

Below are calculations of major health plan stock price growth over a 37 quarter period between May 15, 2009 and September 28, 2018. Note that, during this time, the big plans’ stock price value skyrocketed between 585% and 1,072%, about 2.75x the growth of the Dow Jones Index and 2.25x the growth of the S&P. Humana and United have sustained a breathtaking average per quarter growth of 29.0% and 26.1% respectively.

While stock price is driven by many factors, including historical and expected profitability, these data clearly reflect the truth that health plans earn more if health care costs more. The plans have no reason to remove important element that inflate cost – e.g., low value network providers or unnecessary/inappropriate care. The overarching incentive within the current model is to facilitate more care and more expensive care.

A corollary of these dynamics is that the major plans’ financial performance is undermined by approaches that drive down cost. Restructuring to identify and scale high value services is not an option because total spend would surely drop, dragging earnings, stock price and market capitalization down with it.

The plans can make hay while the sun shines and use that largess to buy into other more currently vibrant lines of business. Even so, they know they’re in a box, stuck trying to maintain a volume-based, low value system in a market that is increasingly adamant about searching for and buying high value.

Major health care newcomers, especially those with heavily diversified interests like Walmart and Amazon, are not saddled with the legacy firms’ perverse constraints, which lends them a strong advantage in a market susceptible to alternatives. Unlike incumbents, they don’t depend on doing the wrong things in health care to prop up market value. They can win by driving better value.

All this suggests there’s a way out of our excruciating health care dilemma. The old guard will be hard pressed to maintain in a market that seeks value, especially when powerful new aggregators appear capable of stepping into the breach and an army of capable risk managers delivers superior results in an array of high value niches.

But that approach depends on high performing vendors convincing self-funded health care benefits managers and their advisers to go around the conventional health care management approaches that have led to ever increasing costs over decades. To succeed, vendors will need to make offers that purchasers can’t refuse. We’ll focus on what that might look like in a future column.

Brian Klepper is The Validation Institute’s Executive Analyst and Editor.